Pricing Phase 1 CORSIA Credits: What to Expect in 2026

Introduction As the aviation sector moves deeper into Phase 1 of the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), the question of credit pricing is becoming increasingly urgent. Airlines need to offset emissions growth above a baseline set at 85% of their 2019 emissions, and corporate buyers across sectors are watching closely—because CORSIA’s […]

-

by Jerome Glass - Article

- Publié le 12/12/2025

Introduction

As the aviation sector moves deeper into Phase 1 of the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), the question of credit pricing is becoming increasingly urgent. Airlines need to offset emissions growth above a baseline set at 85% of their 2019 emissions, and corporate buyers across sectors are watching closely—because CORSIA’s demand could impact the broader carbon market.

But this is not a typical compliance market. CORSIA is subject to major supply and demand uncertainties, driven by host country authorizations, voluntary enforcement, air traffic growth, and regulatory decisions. These uncertainties create significant price volatility, making it a difficult case for procurement managers. CORSIA lacks liquidity, transparency, and predictability. For buyers, this means that timing, strategy, and policy awareness will be critical to managing cost and risk.

This article offers an expert view of where prices stand, what’s driving them, and what to expect in 2026. Whether you’re in aviation or another sector, the goal is to help you anticipate market movements and make informed decisions.

2024–2025 Prices: A Quiet Start, But Signals Emerging

The first CORSIA Phase 1 credits became available in late 2024 through Guyana’s jurisdictional REDD+ program, with an auction price of $21.70 per ton. Eleven airlines participated, purchasing 400,000 credits—less than 3% of the 15.8 million available. Subsequent procurement rounds in 2025 showed a modest upward trend in pricing: credits sold in Q1 were priced at $22.25/tCO₂e, followed by Q3 transactions at $22.55/tCO₂e, according to the International Air Transport Association (IATA).

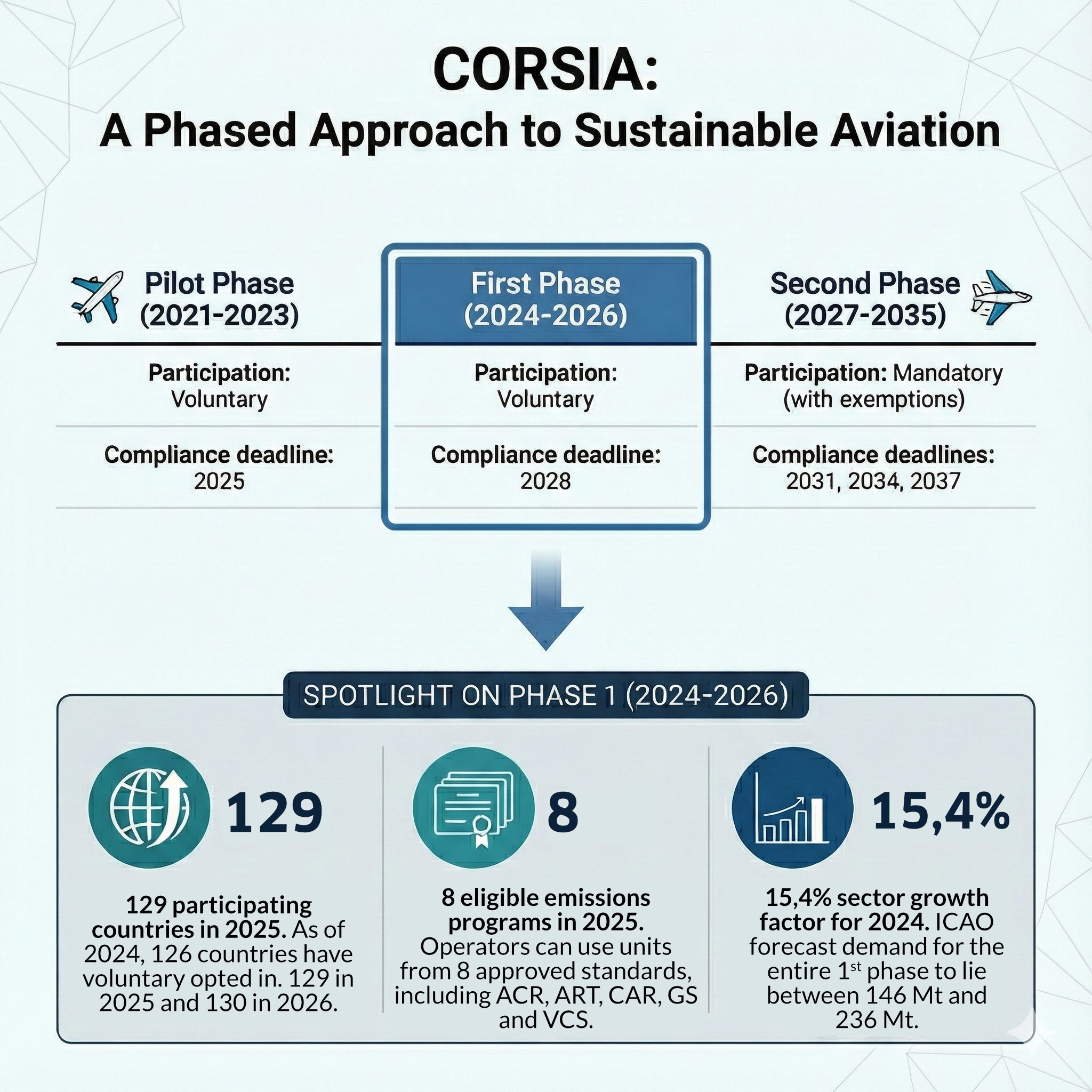

This tepid start reflected market hesitancy. Airlines were cautious, waiting for more clarity on supply, enforcement, and future demand. Meanwhile, the International Civil Aviation Organization (ICAO) approved two new standards in October 2025 (bringing the total number of eligible programs to eight) and reinstated two Verra legacy cookstove methodologies, expanding the theoretical pool of eligible projects. But most of the projects still lack host country authorization.

By the end of 2025, the market prices remained in the low $20s, with limited secondary trading and no clear price trend. The market was in a holding pattern, awaiting stronger signals from regulators and airlines.

Key Market Drivers: What Will Shape Prices in 2026?

Supply Constraints: Host Country Authorization Bottlenecks

The biggest bottleneck is not project availability—it’s government action. Credits must be authorized by host countries and adjusted against their national climate targets through a formal Letter of Authorization (LoA) and a corresponding adjustment (CA). To mitigate the risk that a host country might later revoke its LoA or fail to apply the adjustment, project developers are now required to secure insurance from approved insurance providers.

As of late 2025, only the Guyana jurisdictional REDD+ project and a 1.5-million-credit clean cookstove project in Malawi (under Gold Standard) had completed this process. Other countries are moving slowly, constrained by technical capacity, political caution, or unclear procedures. If only a handful of countries issue credits by 2026, supply will remain tight, pushing prices upward. If more countries are ready to issue LoA and apply CA under Article 6, supply could ease significantly. The pace of government readiness—influenced by political willingness, technical capacity, and legal frameworks—will be the decisive factor in shaping market balance.

Demand Uncertainty: Compliance Levels and Emissions Growth

CORSIA Phase 1 remains voluntary, with 129 countries participating as of 2025. However, enforcement varies widely. While the United States is listed among participants, unlike China and India, its actual commitment to the scheme is uncertain. Only a small number of countries, such as the UK, are working to integrate CORSIA obligations into national legislation (with penalties of £100/tCO₂e).

At the international level, there are no penalties set for non-compliance. As a result, actual demand depends not just on participation but on enforcement. If only a subset of airlines procure credits, demand will be lower. If most comply, demand could lie between 146 and 236 million tons for Phase 1 (IATA forecast August 2025).

Emissions growth also matters. If international air traffic rebounds strongly, credits requirements will rise. Emissions could be 20% above 2019 CORSIA Baseline level by 2025 (2024 Sector Growth Factor being at 15.4%, following ICAO latest revision). A key unknown in 2026 is how international air traffic will behave.

Regulatory Evolution: The EU’s 2026 Review

The European Commission will assess CORSIA’s effectiveness in mid-2026 and will clarify the articulation between CORSIA and EU ETS for intra-EU flights. If the EU sticks with CORSIA, demand will remain strong. If it expands the EU ETS to cover international flights, demand for CORSIA credits could drop significantly.

While an EU exit from CORSIA would have major implications for the scheme’s credibility and the cost burden for airlines, this outcome currently appears unlikely. In the current context, European policymakers seem committed to making CORSIA work effectively, and any adjustments are more likely to involve design changes or deadline extensions. The potential withdrawal of the United States—and the domino effect it could trigger among CORSIA participants—may currently represent a greater point of attention.

Additional Factors: Market Spillover and Article 6

CORSIA credits may increasingly compete with other compliance and voluntary markets. For instance, emerging schemes—like Singapore’s carbon tax—accept international credits which meet specific eligibility criteria and hold corresponding adjustments. As more countries align with Article 6 standards, demand for CORSIA-eligible credits could rise, intensifying competition and driving up prices. This dynamic also introduces the potential for structural price arbitrage between schemes. Different penalty levels and eligibility criteria across jurisdictions could create opportunities—and risks—for buyers navigating multiple markets.

The UN’s Paris Agreement Credit Mechanism (PACM), under Article 6.4, could reshape the market starting in 2026 by transitioning many CDM projects into the new framework. If PACM credits become eligible for CORSIA, supply could improve and ease price pressure. However, ICAO retains authority over eligibility, and delays or restrictive decisions could keep the market tight.

Wrap-up: The Classic Chicken-and-Egg Dilemma

On the supply side, there’s no shortage of projects meeting CORSIA’s quality criteria. The approved standards, methodologies, and projects are already in place. The main constraint is host country authorization. This step is not being held up by paperwork; it hinges on whether governments have clear incentives, such as increased revenue, development opportunities, investment, and access to new technologies.

Projects that clearly deliver these advantages will likely be first on the CORSIA market. Yet those benefits depend on a credible price signal from buyers, creating a classic chicken-and-egg dilemma: without clear demand, governments delay authorization, and without authorization, supply remains limited. How countries navigate this dynamic will define the market in 2026.

Recommendations for Procurement Strategy and Risk Management

For Airlines

- Budget for volatility: Define your budget across a range of price scenarios and complement this with a stress-test on compliance costs and models.

- Start sourcing: Secure credits in 2026 to avoid last-minute premiums. Procure frequently to mitigate the price risk. Use forward contracts, auctions, or bilateral deals. Another option is to enter pre-purchase agreements for conditional CORSIA Phase 1 credits. These deals can offer discounted prices while providing early access to future-eligible credits, though they require careful due diligence on project status and authorization timelines.

- Monitor policy: Track the EU and US decisions, host country authorizations, and ICAO updates. Regulatory shifts will affect demand and pricing.

- Diversify strategy: Invest in operational efficiency to reduce procurement needs and explore sustainable aviation fuel. Consider blending compliance and voluntary credits for flexibility.

For Non-Aviation Corporate Buyers

- Avoid CORSIA credits: Voluntary buyers do not need corresponding adjustments and should avoid competing with airlines for the same credits. CORSIA demand could drive prices up and reduce availability of the CORSIA-eligible credits.

- Procure differently: Focus on jurisdictions and project types not targeted by airlines. Prioritize removals, high co-benefit projects, and credits outside the CORSIA-eligible pool.

- Monitor CORSIA closely: Track developments to anticipate market shifts. If CORSIA demand surges, voluntary buyers may need to adjust sourcing strategies to avoid price pressure or supply constraints.

- Protect ESG integrity: For airlines, CORSIA represents the sector’s view to ESG credibility. However, ESG integrity may differ across other sectors and companies, where voluntary frameworks and priorities vary. Establishing clear benchmarks tailored to your company is essential for credibility and resilience.

For All-Sectors

- Engage with suppliers: Maintain active relationships with carbon credit suppliers. Early engagement can secure better terms.

- Leverage intelligence: Use market trackers, policy briefings, and industry networks to stay ahead of developments. Information is a strategic asset.

- Communicate internally: Ensure finance and leadership teams understand the potential cost exposure. Carbon procurement is a strategic lever, not a compliance afterthought.

Final Thought

CORSIA’s Phase 1 credit market is entering a decisive phase. Prices in 2026 will reflect the interplay of supply readiness, airline behavior, and regulatory choices. For corporate buyers, the key is to stay informed, act early, and manage risk proactively.

But with current market uncertainties, different procurement strategies will lead to very different results. Timing, sourcing, and policy awareness will define success. Monitoring developments—especially the EU’s 2026 review, host country authorizations, ICAO announcements, and signals from the U.S. and China—is essential. Buyers must be ready to pivot as conditions evolve.

Whether you’re in aviation or another sector, the message is clear: carbon credit procurement is not a compliance checkbox—it’s a strategic lever to manage risks and capture opportunities. And in the CORSIA market, agility, insight, and execution will make all the difference.