Blue Carbon 101: Why Mangroves Matter and What Buyers Should Look For

-

by Nathalie Wijns - Article

- Publié le 01/04/2026

Author: Jihane LEBAS GUENOUN, Originator for ENGIE Global Markets, Carbon Desk

When thinking about carbon capture and storage, forests often come to mind as the world’s main natural carbon sink. Yet the ocean plays an even larger role, capturing more than half of all biological carbon through organisms ranging from phytoplankton to coastal ecosystems such as mangroves. This reality is often overlooked in climate discussions, yet it underpins a promising, if sometimes misunderstood, segment of the voluntary carbon market (VCM): Blue Carbon.

This article explores how VCM buyers can navigate the emerging Blue Carbon space and identify high-quality credits with a focus on mangrove carbon projects—the most established category of Blue Carbon today. As with other segments of the VCM, Blue Carbon’s promise is accompanied by legitimate integrity risks, making careful project evaluation essential as this market develops.

What counts as Blue Carbon?

The term “Blue Carbon” was introduced by Christian Nellemann and colleagues in a 2009 report highlighting the need for coordinated efforts to conserve and restore marine ecosystems. It helped spark international interest in using market mechanisms to manage these ecosystems which reduce greenhouse gas emissions and increase carbon sequestration.

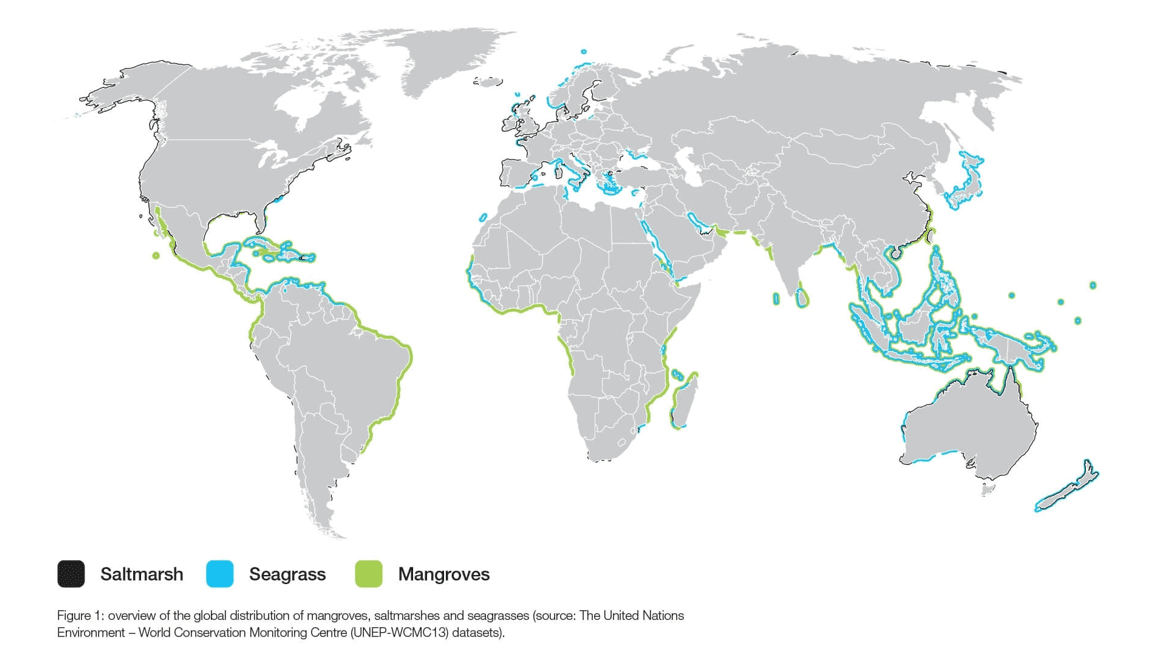

The IPCC currently considers three ecosystems to fall under this definition: mangroves, seagrass meadows and tidal marshes, which are referred to as Coastal Blue Carbon Ecosystems.

Coastal Blue Carbon ecosystems are compelling because they can store between two and five times more carbon per hectare than terrestrial forests. They cycle nearly the same annual amount of carbon as terrestrial ecosystems despite representing only about 0.05 percent of global plant biomass. This combination of high sequestration potential and relatively limited land competition compared to other natural solutions makes them particularly relevant for climate mitigation.

Despite several global initiatives aiming to protect them, funding remains insufficient to support long term conservation and restoration of these ecosystems. The VCM can help address this gap.

Even though Blue Carbon credits represent less than 1 percent of global issuances, they offer buyers an opportunity to diversify portfolios, diversify risks, and support one of the most climate critical ecosystems on the planet. Among these, mangrove projects dominate current supply.

Newly-planted mangroves establishing root structure. Survival rates in the first 2–3 years are a key performance indicator for restoration‑based credit quality.

Mangroves and their role in Blue Carbon ecosystems

Mangroves are coastal forests of trees and shrubs found along tropical and subtropical coasts and estuaries. Their aerial root systems trap sediments and create ideal conditions for slow decomposition, enabling long-term storage of large volumes of carbon in biomass and soils, a key driver of their sequestration potential.

Mature mangrove stands with decades‑old root systems, the conditions under which deep, stable soil carbon stocks accumulate. Baseline assessments in these areas underpin long‑term carbon storage potential.

Globally, mangroves cover an estimated 14.8 million hectares, with over one‑third concentrated in Southeast Asia and over 20% in Indonesia alone. This geographical distribution matters for the VCM: it concentrates project opportunities in countries where land‑tenure clarity, community ownership, and governance conditions play a decisive role in permanence and delivery.

Mangroves are also the most established of all Blue Carbon ecosystems. Studies indicate they store an average of 394 tonnes of carbon per hectare in biomass and the top meter of soil, with some systems reaching 650 tonnes.

Beyond carbon: socioeconomic and ecological value

One reason high-quality mangrove restoration and conservation projects have gained traction among carbon buyers is that their climate mitigation potential comes with quantifiable ecological and socioeconomic cobenefits. Mangroves protect coasts by reducing erosion, buffering storm surges, and lowering disaster recovery costs for the more than 200 million people living near these ecosystems. Regions that saw extensive mangrove clearing in the twentieth century often experienced coastline retreat and increased community displacement, illustrating the material risks avoided when these ecosystems remain intact.

From a biodiversity standpoint, mangroves rank among the most productive ecosystems globally, providing critical nursery habitats for commercially important fish and crustaceans, as well as supporting species found nowhere else.

Abandoned houses following mangrove clearance and subsequent coastal retreat in Indonesia in the 1970s, a reminder of the beyond-carbon value of conserving and restoring these ecosystems.

Key considerations when buying mangrove carbon credits

Mangrove projects differ from terrestrial forest projects not only biologically but operationally, institutionally, and socially. Mangrove carbon credit buyers should pay close attention to several categories of risks when assessing their quality.

1. Limited supply of projects

While studies estimate that around one million hectares of mangroves could be restored or conserved through carbon finance, only around 100 Blue Carbon projects are currently registered, and just a small share of those have issued credits, mostly from Southeast Asia. Buyers therefore face a narrow set of available options and may need to consider projects still under development, which inherently carry higher risks.

2. No CCP-approved mangrove methodology yet

In addition to project scarcity, there is currently no mangrove-specific methodology approved under the ICVCM Core Carbon Principles. Only Isometric and Gold Standard methodologies have entered the early stages of ICVCM’s assessment, meaning buyers cannot yet rely on CCP alignment as a screening tool for high-integrity projects.

3. Access constraints and delivery risks

Mangroves are often located in remote areas accessible only by boat or on foot, where deep mud and highly variable tides complicate planting, monitoring and verification. When project teams lack adequate equipment or staff, these constraints can delay implementation and affect credit delivery schedules and project finances. Before committing, look for evidence of operational planning and budgeting that reflect these realities.

A restoration site adjacent to traditional fishing areas: project success depends on aligning carbon sequestration goals with local livelihood benefits

4. Unclear land tenure and social safeguard considerations

Mangrove areas often lack clear land tenure and are subject to overlapping mandates from maritime authorities, forestry agencies, and agrarian ministries, particularly in accretion zones where newly-formed land formed may not appear in cadastral records and have no formally recognized ownership.

In this context, a detailed assessment of land use, access rights and traditional or informal tenure is essential. Buyers should seek evidence that all rightsholders have been identified and meaningfully consulted, provided consent, and that resource rights are safeguarded.

For projects to endure, buyers must understand local governance systems and, in some cases, adapt their expectations to customary arrangements.

5. Anthropogenic pressure and permanence risks

Historic mangrove loss has largely resulted from conversion to aquaculture, industrial development and, in some regions, fuelwood harvesting. Buyers should evaluate whether project activities address these drivers and whether site selection mitigates future risk by accounting for economic pressures, land use patterns, long-term community needs, and ecological suitability.

Natural regeneration occurring in former aquaculture ponds: a promising signal, but one that requires verification that the economic drivers of past conversion have been addressed

6. Sea level rise and natural permanence risks

Mangroves can adapt to moderate sea-level rise through sediment accumulation, but this capacity varies significantly by site and is not guaranteed. Buyers should ensure projects adequately demonstrate that restored areas are likely to remain resilient given local sea-level rise projections, hydrology and soil characteristics.

7. Soil carbon uncertainty and evolving scientific understanding

Despite advances in monitoring tools and methodologies that may suggest otherwise, understanding of carbon accumulation in mangrove soils remains limited and highly variable. Buyers should therefore look for projects that apply conservative assumptions, robust sampling designs, and site-specific data rather than relying on generalized models.

From potential to impact: Due diligence for high-quality mangrove credits

Blue Carbon markets, and mangrove projects in particular, represent a critical nature-based solution with significant untapped potential. They offer strong climate mitigation benefits and vital ecological and socioeconomic value for coastal communities. Yet navigating this market requires attention to land tenure complexities, delivery risks linked to difficult logistics, and both anthropogenic and natural permanence risks.

The strongest mangrove projects will not be the ones that promise the largest maps or the most optimistic volumes. They will be the projects that demonstrate deep understanding of local governance, hydrology, and community priorities, and that show how their operations adapt to the realities of tides, soils, access constraints, and long-term stewardship.

As buyers enter the Blue Carbon market, shifting the focus from theoretical potential to feasibility and legitimacy will be essential. When selected with this mindset, mangrove credits can strengthen climate impact, increase portfolio resilience and support one of the most valuable ecosystems on Earth.