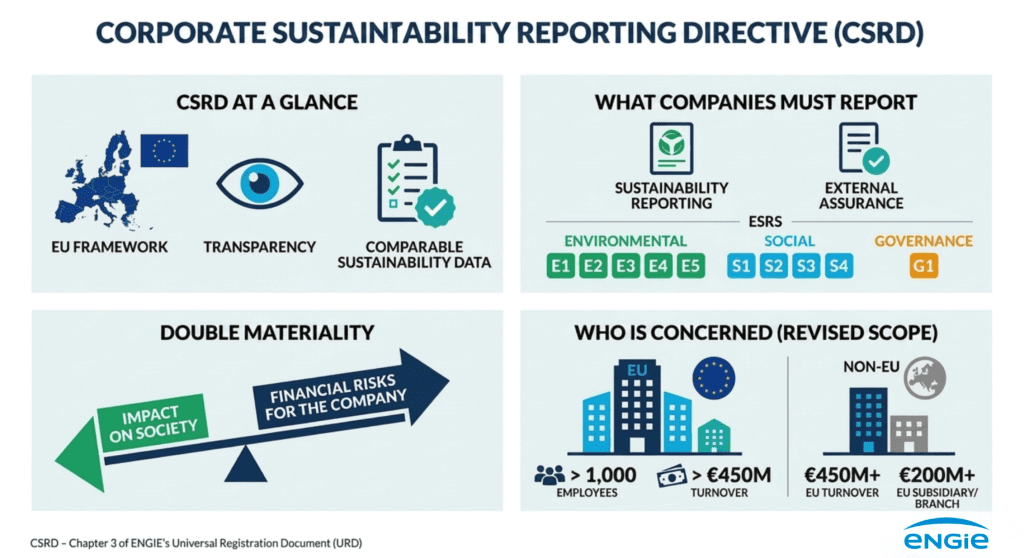

What is the CSRD?

The CSRD was officially adopted by the European Union Council and entered into force on January 5, 2023, replacing the previous Non-Financial Reporting Directive (NFRD) with stricter, mandatory requirements. The implementation of the CSRD is also intented to strengthen corporate accountability regarding environmental, social, and governance (ESG) issues. The directive mandates that companies to disclose their governance structures, the effectiveness of their sustainability strategies and their approaches to risk management in relation to ESG factors.

The first companies subject to the CSRD had to apply the new rules for the first time in the 2024 financial year, for the sustainable statement published in 2025.

Major update: The Omnibus I Simplification Package (2025–2026)

The CSRD has been significantly revised since its original adoption. In December 2025, the European Parliament approved sustainability-related changes as part of the Omnibus I simplification package, which significantly narrowed the scope of the CSRD.

Directive (EU) 2026/470, covering the proposed changes to the CSRD and the Corporate Sustainability Due Diligence Directive (CS3D), was published in the Official Journal of the European Union on 26 February 2026. EU member states now have until March 19, 2027 to transpose the CSRD changes into national law.

Revised scope: which companies must comply?

The revised CSRD now applies primarily to the largest companies. Only companies with more than 1,000 employees and over €450 million in net annual turnover, with numbers consolidated for EU-incorporated parent companies,remain in scope.

For non-EU companies, the rules are largely the same: non-EU companies must comply if they have a net turnover of €450 million or more in the EU, and their subsidiaries or branches must comply if they have a turnover of €200 million or more in the EU.

The double materiality principle

A key element of the CSRD is the double materiality principle, which requires companies to report on two dimensions:

1. Financial materiality – the risks sustainability issues affect the company’s financial performance (such as rising energy costs or resource scarcity).

2. Impact materiality – the impacts a company’s operations have on the environmental and social factors (such as CO₂ emissions, biodiversity loss and labor practices).

By addressing both dimensions, businesses gain a more comprehensive understanding of their operations, enabling them to manage risks and identify opportunities more effectively.

European Sustainability Reporting Standards (ESRS):

In response to the needs of businesses for clear guidance on reporting, the European Financial Reporting Advisory Group (EFRAG) has developed the European Sustainability Reporting Standards (ESRS). These standards aim to provide detailed metrics that organizations must report to comply with the CSRD. The ESRS encompasses various categories, including general disclosures, environmental impacts, social workforce factors, and governance policies.

The four primary categories of the ESRS, namely cross-cutting, environmental, social, and governance, outline a robust framework for corporate sustainability disclosures. Cross-cutting disclosures require organizations to provide general information about their sustainability policies, governance structures, and overall objectives related to ESG. Environmental disclosures necessitate in-depth analysis focusing on issues like climate change, water and marine resources, biodiversity and pollution.

Social disclosures recognize the importance of examining not only internal workforce dynamics but also the impact of organizations in their surrounding communities and supply chains. Governance disclosures provide insight into how companies are steering their sustainability initiatives, highlighting accountability and strategic alignment.

Benefits of CSRD reporting:

Beyond compliance, the CSRD brings clear benefits for companies. It improves transparency by requiring consistent and comparable sustainability information, which helps build trust with investors, lenders and other stakeholders. By integrating sustainability into strategy and governance, the CSRD also helps companies better identify risks and support long-term value creation.